A Budget is a pre-planned monetary report that clarifies how future income and expenditure will be determined thing astute. Budgeting is a management tool for planning and controlling future financial activities. Here in this article, we have explained what is budget and its meaning, definition, types, and objectives.

► What is a Budget?

Budgeting is an operational plan for a definite period usually a year, expressed in financial terms and based on the expected income and expenditure.

For Example, Union Budget in parliament every year details the government plan for taxation and spending in the coming financial year. The Finance Minister of presenting the Union Budget.

◉ Budget Meaning

- A budget means a pre-determined plan of financial terms.

- It is prepared for a definite time period.

- The act of preparing a budget is called budgeting.

◉ Definition of Meaning

A budget has been defined as “a blueprint of a projected plan of action of a business for a definite period of time.”

“Budgeting is a concrete precise picture of the total operation of an enterprise in monetary terms.” – H.M. Donovan

“A budget is a financial and quantitative statement, prepared and approved prior to a defined period of time, of the policy to be pursued during the period for the purpose of attaining a given objective.” – ICMA England

“The budget may be defined as a predetermined detailed plan of action developed and distributed as a guide to current operations and as a partial basis for the subsequent evaluation of performance.” – Gordon Shillinglaw

“The budget is a process consisting of a series of activities relating expenditures to a set of goals.” – Allan Schick

► Objectives Of Budget

- Resource reallocation.

- Pay and abundance reallocation

- Public-area the board

- Financial Stability

- Financial Development

- Business Creation

► Types of Budget

- Master Budget

- Flexible Budget

- Static Budget

- Rolling Budget

- Zero Based Budgeting

► Examples of Budget

- Capital Budget

- Expense Budget

- Cash-flow Budget

- Financial Budget

- Operating Budget

- Labor Budget

- Production Budget

- Sales Budget

► Preparation of budget

Budgets are essentially short-term plans which help to achieve the long-term objectives of the business. There are various steps involved in the preparation of the budget.

- Define major Goals & Objectives (Develop financial plans & policies)

- Gather Data (Access Historical records and actual data)

- Prepare the Model (Develop Base Budge and drafting)

- Approval of the budget (Review of the budget)

- Communicate the Budget

- Report interim result

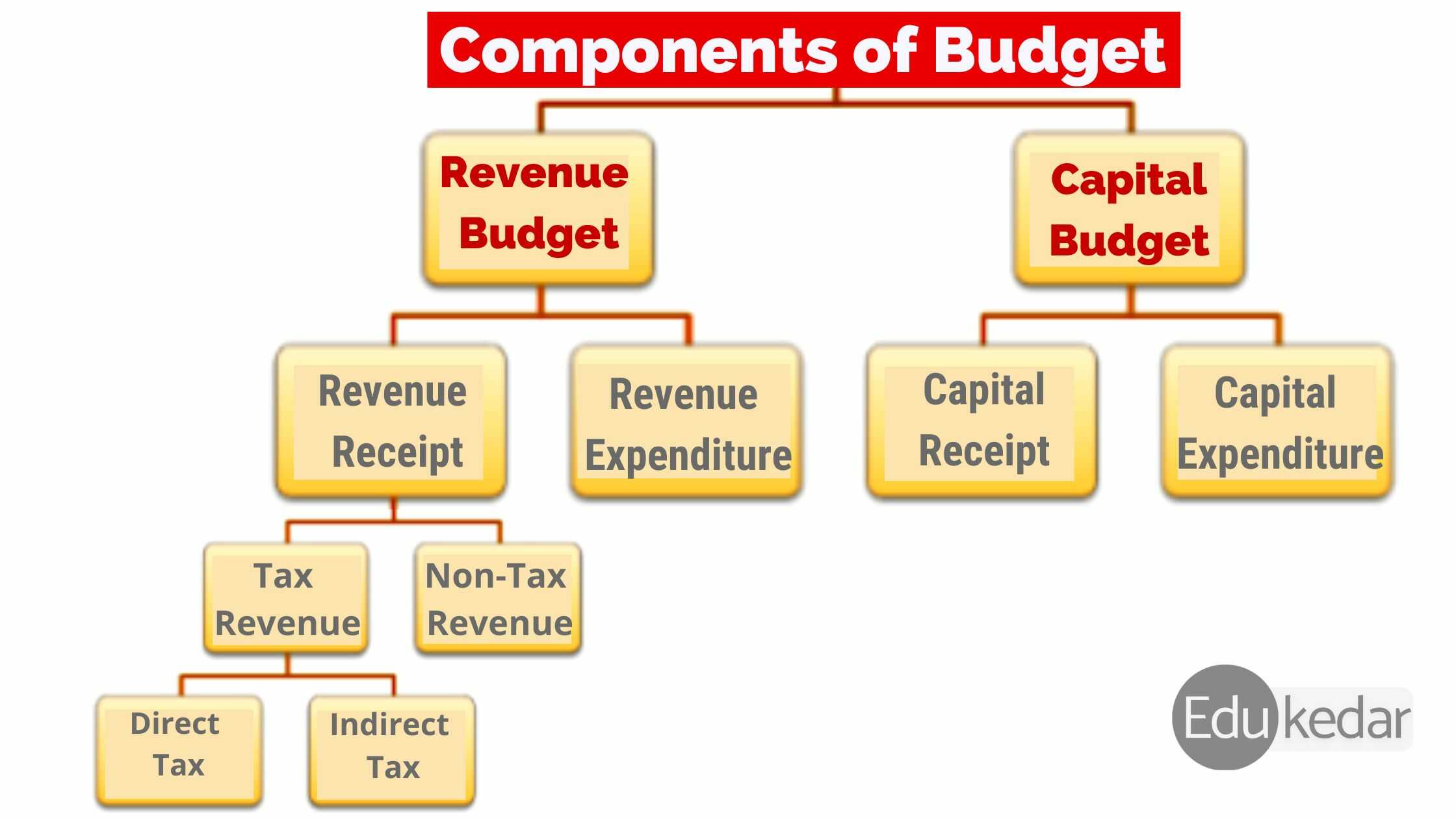

► Components of Budget

There are two components of the budget that are as follows;

- Revenue Budget

- Capital Budget

► Revenue Budget

In Revenue Budget, the income financial plan is comprised of the public authority of India’s income receipts and the uses that are met with that income.

- Revenue Receipts

- Revenue Expenditure

◉ 1. Revenue Receipts

Revenue receipts are those that don’t bring about an obligation or a decline in resources. The income is then parted into two classifications.

✔ Receipt from Tax

- Direct Tax

- Indirect Tax

a. Direct Tax

A citizen covers direct duties to the public authority. It is additionally described as an assessment wherein the singular bears both the obligation and the weight of installment. As per the sort of expense charged, both the focal government and state legislatures gather direct duties.

b. Indirect Tax

The end customer of items and administrations is eventually answerable for backhanded expenses. It is difficult to stay away from in light of the fact that charges are exacted on the two items and administrations. It involves lower authoritative expenses because of advantageous and standard assortments.

✔ Receipt from Non-Tax:

These incorporate interest, business income, outside awards, fines, punishments, etc.

◉ 2. Revenue Expenditure:

The idea of income use is for the most part current or present moment. They are costs that the public authority should cause to do its everyday activities.

These expenses are completely energized in the year they are brought about and do not deteriorate over the long run. They may either be repeating or non-repeating.

Also Read :Basics of Accounting

► Capital Budget

In Capital Budget, capital receipts and expenditures are considered for the capital financial plan. It additionally incorporates exchanges from the Public Account.

- Capital Receipts

- Capital Expenditure

◉ 1. Capital Receipts

Capital receipts are government receipts that make risk or drain monetary resources. The primary wellsprings of capital receipts are advances from people in general, otherwise called market borrowings.

Borrowings from the Reserve Bank, business banks, and a few other monetary establishments through the offer of depository charges, borrowings from unfamiliar legislatures and global associations, and credit recuperations.

Little investment funds, opportune assets, and net receipts from the offer of offers in Public Sector Undertakings are among the different things (PSUs).

◉ 2. Capital Expenditure:

Capital consumptions are one-time ventures of cash or capital made by an administration for the point of growing in different areas and organizations to make benefits.

These assets are regularly used to get fixed resources or resources with a more extended life expectancy. These incorporate hardware, producing gear, and framework improvement gear.

These resources offer some incentive to the public authority during their whole life expectancy and could possibly have rescue esteem.

► Budget Deficit

“A budget deficit is an amount by which the income of any business or government falls short of the expectations set forth in its budget over a given time period.”

The budget deficit is the term used to define the situation when expenditures exceed revenue. It occurs when Government spends more than they get from revenue.

- Budgetary deficit is the sum of revenue account deficit and capital account deficit.

- If revenue expenses of the government exceed revenue receipts, it results in a revenue account deficit.

- Similarly, if the capital disbursements of the government exceed capital receipts, it leads to a capital account deficit.

- The budgetary deficit is usually expressed as a percentage of GDP.

◉ Measures of Budget Deficit

- Revenue Deficit

- Fiscal Deficit

- Primary Deficit

✔ 1. Revenue Deficit

The revenue shortfall is characterized as the distinction between complete income gathered and absolute income consumption. Just current pay and current costs are remembered for this shortage.

A huge shortage figure suggests that the public authority ought to lessen its spending. The public authority might have the option to support income by raising assessment income.

Revenue Deficit = Total income consumption – Total income receipts.

Implications of Revenue Deficit are:

- A huge income setback demonstrates monetary indiscipline.

- It demonstrates that the public authority is dissaving, i.e., the public authority is using reserve funds from different areas of the economy to pay for its customer consumption.

- It demonstrates that the public authority is dissaving, i.e., the public authority is using reserve funds from different areas of the economy to pay for its customer consumption.

- It shows the public authority’s inordinate consumption of the organization.

- It brings the public authority’s resources owing down to disinvestment.

- A huge income shortage conveys an admonition message to the public authority to either cut spending or lift income.

✔ 2. Fiscal Deficit

A monetary shortage happens when the public authority’s complete consumptions surpass its whole income created. The public authority’s borrowings, be that as it may, are excluded.

Fiscal Deficit = Total consumption – Total receipts barring borrowings

Implications of Fiscal Deficits are:

- A huge downside or outcome of financial shortage is that it might bring about an obligation trap.

- It causes inflationary tensions.

- It smothers future headway.

- It expands dependence on unfamiliar assets.

- It raises the public authority’s commitment.

✔ 3. Primary Deficit

It is inferred by taking away interest installments from the financial shortage.

Primary Deficit = Fiscal shortfall – Interest installments on past advances

Implications of Primary Deficit:

It reflects the number of the public authority’s borrowings that will be utilized to take care of expenses other than interest installments.

Measures to Correct Different Deficits:

- Government endowment cuts will support decreasing the shortfall.

- Where resources are not being utilized proficiently, disinvestment ought to be completed.

- Expanded accentuation on charge-based incomes, just as vital stages to forestall tax avoidance.

- Acquiring from both homegrown and worldwide sources.

- A more extensive expense base could likewise support the decrease of the public authority’s shortage.

► What is Fiscal Policy?

Fiscal policy is an important tool at the disposal of the Government to influence the economic growth of the nation based on Keynesian economics. It is used in coordination with monetary policy.

- Fiscal Deficit: If the government spends more than what it earns it leads to a deficit.

- Fiscal Surplus: If the Government spends less than what it earns, it creates a fiscal surplus.

Keynesian Economics is all about promoting government spending on infrastructure, employment benefits, and education to increase consumer demand.

This theory argues that government spending is necessary to maintain full employment. It shows us the potential of fiscal policy as a tool capable of reducing fluctuations in demand.

When an economy is operating below its potential output, the Keynesian model suggests that the government should use expansionary fiscal policy by increasing the government purchase of goods and services or cutting taxes.

◉ Debt

An amount of the cash acquired by one substance, the borrower, from another element, the banks, is alluded to as an obligation.

State-run administrations acquire cash to cover their deficiencies, which permits them to finance standard tasks just as huge as capital consumption. This obligation may be as a credit or bond issuance.

► What is Monetary Policy?

Monetary policy has been defined as the actions central banks take to achieve objectives such as price stability (control inflation) and maximum employment

In India Monetary policy is decided by the Central bank “Reserve Bank of India”.

- Control money supply

- Raises/Lows the bank rate/repo rate.

- Works faster than fiscal policy

- Helps in maintaining efficiency.

{kind=link}